The 2026 Iran conflict is reshaping the risk outlook for Australian general insurers. Pressures that are usually analysed separately are now converging, compounding an affordability crisis at least five years in the making with effects likely to outlive the conflict itself. As volatility becomes the new norm, understanding and adapting to this new risk landscape will determine who thrives.

For many Australian households, insurance has now become one of the largest non‑discretionary expenses – home premiums are up almost 70%*, 15% of households are in affordability stress, the RBA has hiked rates twice in 2026 already, and heightened claims inflation will likely outlast the conflict. For insurers, that pressure no longer sits only in claims costs. It is reshaping demand, investment risk, capital adequacy and portfolio composition at the same time.

The 2026 Iran conflict is escalating these pressures through three risk channels simultaneously:

- An energy and supply chain shock driving broad-based claims inflation

- Macro and financial market stress impairing investment returns

- Conflict activity – vessel attacks, airspace closures, cyber threats and proxy operations – generating elevated risk exposures across specialty lines and beyond.

The real challenge for Australian insurers lies not just in tackling each risk on its own, but in managing the combined impact. Insurer success now hinges on recognising how these risks are interconnected and adapting strategies for a world where volatility is the new norm.

So, what does this mean for general insurers in practice? We examine how each risk channel is affecting the industry and outline the actions insurers must take to navigate the rapidly changing landscape.

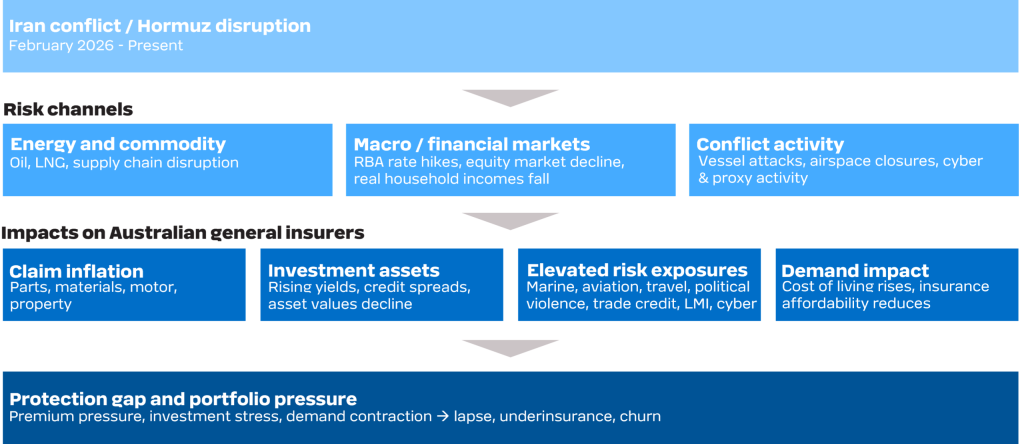

Tracing risks, from conflict to the impact on Australian insurers

The conflict flows through three risk channels – each generating distinct impacts on Australian general insurers. The figure illustrates the interplay between these risks and the impacts on general insurers.

Now we explore how each of these risks translates into impacts on general insurers in more detail.

1. Claims inflation – Beyond the bowser

Australian general insurers are facing widespread claims inflation. Australian petrol prices rose around 70 cents per litre to their peak in March with the government’s temporary excise halving clawed back approximately 26 cents, but prices remain around 40 cents above pre-conflict levels. Diesel has climbed above $3 per litre, with the divergence particularly acute for transport, farming, and construction.

Supply chain disruption adds a second layer. Freight surcharges have been in place since early March, and disruption to global shipping routes is flowing through to the cost of goods underpinning claims – vehicle parts, building materials, plant and equipment. Preliminary ICA data shows cost increases of up to 36% for building materials, 30% for trades and on-site specialists, and 50% for freight.

The result is broad-based claims cost pressure across almost all classes, driving up average claim sizes and, in turn, premiums.

2. Investment assets – When duration matching falls short

Rising energy and supply chain costs are pushing up claims inflation – and the RBA is responding with rate hikes. Higher rates reduce the market value of fixed interest securities. Interest bearing securities comprise over 80% of direct insurer assets* and over 95% of reinsurer assets*. Where duration matching is sound, falling bond values are offset by a corresponding fall in the present value of liabilities but this only addresses the discount rate effect. Claims inflation independently increases the nominal value of future liability cash flows, pressuring the balance sheet from both sides. Inflation-linked bonds offer a partial hedge in principle but limited market depth constrains their use at scale – and CPI may not move in sync with the specific cost pressures driving claims inflation in motor, property, and other lines.

Beyond liability-backing assets, surplus capital deployed in fixed income or equities has no natural hedge. The ASX fell more than 7% through March. For direct insurers with meaningful equity exposure, the capital impact is even more significant.

3. Elevated risk exposures – Performance of specialty lines and beyond

Direct exposure to conflict-sensitive specialty classes for Australian general insurers is limited, with globally mobile risks – including international marine hull, airline aviation war and allied perils, and political violence – largely placed through the London market.

Impacts are more likely to be indirect. In cyber, the conflict is contributing to an elevated global threat environment, including increased state-linked activity, with potential implications for underwriting and losses. The macroeconomic spillover is also elevating risk in other lines – most notably LMI – where inflation and a tightening RBA bias are weighing on housing demand, with clearance rates at multi-year lows and employment expected to soften.

4. Demand impact – Affordability and attrition

Affordability pressure is reshaping customer behaviour across the market in four ways.

| Behaviour | Customer action | Insurer impact |

|---|---|---|

| Lapse | Cancel cover entirely – over 340,000 homes already uninsured, around half citing cost (Australia Institute, 2025) | Premium volume falls; portfolio risk composition may shift as customer mix changes |

| Underinsurance | Reduce sum insured to lower premium – over 530,000 households already underinsured (Australia Institute, 2025) | Shortfall disputes and reputational damage at point of claim |

| Product substitution | Migrate to narrower, lower-cost covers | Revenue mix deteriorates; coverage adequacy falls across the portfolio |

| Active shopping | Increase comparison activity and churn | Margins erode; acquisition costs rise |

Premium affordability and insurability has risen from the sixth most commonly reported business challenge in 2025 to the first in 2026.

Gallagher Bassett Carrier Perspective: 2026 Claims Insights sneak peek

How the industry needs to respond

The conflict is forcing a fundamental reset across planning, capital and operations. Across the industry, five clear priorities are emerging in response.

Looking Ahead

Structural shocks that generate correlated, simultaneous pressure across claims, assets, and demand are not a one-off feature of 2026 – they are an increasingly consistent feature of the risk environment. This time it was Hormuz and energy, next time it could be another regional conflict disrupting technology supply chains, a major climate event tightening reinsurance capacity, or something else entirely. The challenge is not predicting the next crisis, it is building the infrastructure and processes to respond rapidly when the next trigger arrives. These include scenario frameworks that can be reoriented quickly, assumptions built to be updated rather than anchored to history, and capital and portfolio positions that are monitored against a range of outcomes. Insurers who invest in this capability now will be better placed to navigate whatever comes next.

* Based on Taylor Fry’s analysis using the Australian Prudential Regulation Authority’s quarterly general insurance performance statistics for December 2025.

** https://www.fcai.com.au/evs-surge-as-buyers-respond-to-fuel-uncertainty/